I. Overview of the Hydrogen Peroxide Market in 2025

In 2025, the market price of hydrogen peroxide in China showed a trend of "low at first and then high". Although the average annual price has decreased compared with previous years, its profit situation is still considerable compared with many chemical products. In the first half of the year, the market operation was relatively weak. However, in the second half of the year, with the strong demand for papermaking and new energy, prices showed an overall upward trend. By the end of the year, it is expected to end with a "tail-end" rally. Looking forward to 2026, with the successive commissioning of new production capacity and the simultaneous growth of downstream demand, the situation of oversupply in the market will continue. However, the vigorous promotion from the policy end may trigger market fluctuations within the region or during specific time periods, presenting a situation where challenges and opportunities coexist in the market.

In 2025, the average price level of the hydrogen peroxide market witnessed a significant year-on-year decline, mainly attributed to the persistently high supply and overall weak demand. Although the average price of hydrogen peroxide has dropped, its profit situation remains superior compared with other chemical products, even exceeding the expectations of industry players. Especially after entering the second half of the year, with the strong recovery of the demand side and the increase in the operating rates of industries such as iron phosphate and papermaking, the price of hydrogen peroxide has shown a phased rise. Therefore, the price trend of hydrogen peroxide throughout the year shows a characteristic of "low at first and then high", and it is expected to end the year with a "tail-end" rally.

▍ Price trend analysis

In 2025, the market price of hydrogen peroxide in China showed a trend of "low at first and then high", with the overall average price dropping significantly year-on-year. As of December 3rd, the average price of hydrogen peroxide with a concentration of 27.5% across the country has dropped to 735 yuan per ton, a decrease of 13.53% compared to 850 yuan per ton in 2024. During the year, the lowest average price of hydrogen peroxide occurred in late February at 671 yuan per ton, while the highest point was in mid-October, reaching 893 yuan per ton, with a price difference of as high as 222 yuan per ton.

In the first half of the year, due to the persistently high operating rates of enterprises and the continuous abundance of supply, while the escalation of the trade friction between China and the United States led to relatively insufficient support from the demand side. Especially after April, the significant decline in the operating rate of caprolactam has had a negative impact on the hydrogen peroxide market. Despite this, the price of hydrogen peroxide was pushed up several times in the first half of the year, such as the overall price increase in East China in March and in Shandong in June. However, the scope and extent of the price increase were both limited.

Since the second half of the year, especially since late August, with the stimulus of purchasing news from large-scale papermaking enterprises, the range of hydrogen peroxide price hikes has gradually expanded from the Central China region to the surrounding areas. Meanwhile, the strong growth in demand for iron phosphate and the production cuts in some regions further drove the continuous rise in hydrogen peroxide prices between September and October. With the improvement of profit conditions, enterprises that have been out of production for a long time have also started to resume work. After the supply volume returned to a high level in November, it slightly declined, but the overall demand support remains strong. Therefore, the price of hydrogen peroxide rose again in December, and the market is expected to end the year with a strong performance.

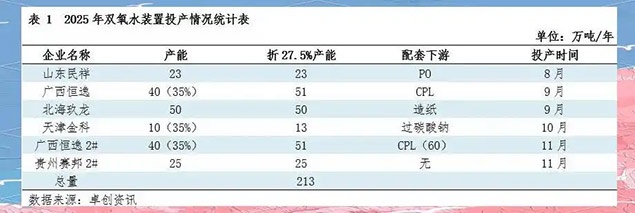

▍ Capacity and supply

In 2025, the growth rate of new hydrogen peroxide production capacity will slow down significantly. Due to the long-term low prices, the commissioning plans of most facilities have been postponed, especially in the first half of the year, when no new production capacity was put on the market. The newly added production capacity within the year was mainly concentrated in the third and fourth quarters. By the end of November, a total of 6 production lines had been put into operation throughout the year, with an additional production capacity of 2.13 million tons per year (calculated at a concentration of 27.5%). Over the past five years, the production capacity and output of hydrogen peroxide have continued to rise. It is expected that by 2025, China's total hydrogen peroxide production capacity will reach 32.33 million tons per year, representing a year-on-year growth of 1.96%. The total output is expected to be 22.2 million tons, with a possible year-on-year increase of 6.27%. From the perspective of enterprise operation, the operation load rate of hydrogen peroxide in 2025 was 68%, up by 1 percentage point year-on-year. Although the number of starts in the first and fourth quarters rose significantly year-on-year, the number of starts in other periods decreased year-on-year. Due to the expansion of the production capacity base and a slight increase in the operating load, the year-on-year increase in supply in 2025 is very significant.

The downstream demand is growing

Over the past five years, the downstream consumption of hydrogen peroxide in China has maintained a steady growth trend. It is expected that by 2025, the downstream consumption of hydrogen peroxide will increase by 6.57% year-on-year, reaching 22.07 million tons. This growth is mainly attributed to the release of new production capacity in downstream products. Meanwhile, the operating rates of multiple downstream product industries have also risen significantly, especially in the papermaking and new energy sectors, where the performance is particularly outstanding. During the year, the new production capacity in the papermaking industry increased significantly, and the operating rate of the iron phosphate industry also continued to set new historical highs, which provided strong support for the demand of hydrogen peroxide.

However, caprolactam, one of the main downstream products of hydrogen peroxide, will face fierce competition within the industry in 2025, with multiple production cuts and capacity reductions within the year, which will have a limited boosting effect on the demand for hydrogen peroxide. On the other hand, propylene oxide, a representative of integrated units, has maintained ultra-low load operation for a long time throughout the year. Most HPPO enterprises have been stably selling hydrogen peroxide externally. Although this has increased supply pressure to a certain extent, the demand boost is still weak.

The new production capacity in the papermaking sector has significantly increased within the year, and the demand growth momentum is strong. Meanwhile, leading paper enterprises that had been out of production for a long time in the fourth quarter resumed operations, further boosting demand. Under the continuous impetus of policies and orders, the construction of the lithium iron phosphate sector has steadily increased within the year, and the load rate has continuously set new highs. Especially in the second half of the year, leading enterprises basically maintained full production capacity, providing strong support for demand in Central China and Southwest China.

Ii. Market Outlook for 2026

Forecast: In 2026, the hydrogen peroxide market will face a complex situation of both increased supply and demand, presenting both opportunities and challenges. In 2026, the hydrogen peroxide market will face both challenges and opportunities amid an increase in supply and demand, and the price may remain at a low level with a narrow range of fluctuations. On the supply side, the actual new capacity put into operation in 2025 was lower than expected. Some facilities are projected to be released in a concentrated manner in 2026, leading to a continuous increase in supply and maintaining the supply pressure. Meanwhile, at the policy level, the elimination of the outdated "acid-base fixed bed" process for hydrogen peroxide is gradually being put on the agenda. As the policy deadlines in some provinces approach, it may lead to temporary supply shortages in certain areas. Based on the progress of new capacity deployment and the renovation of old facilities, it is expected that the output of hydrogen peroxide will continue to grow in 2026, but the growth rate may be limited.

On the demand side, in 2026, the main downstream varieties of hydrogen peroxide such as caprolactam, propylene oxide, chemical machinery slurry, and iron phosphate will all be in the peak period of capacity expansion, and the demand for hydrogen peroxide will continue to increase. It is expected that the demand in 2026 will further rise year-on-year. However, the extent to which the macroeconomic environment and foreign trade recover will remain the key factors restricting downstream demand.

Taking into account both supply and demand factors, the uncertainties regarding the introduction of new production capacity, the renovation and exit of old facilities, and the recovery of terminal demand make the hydrogen peroxide market in 2026 present both opportunities and challenges. The primary driving force influencing the future trend of hydrogen peroxide prices remains the change in the fundamentals of supply and demand. Meanwhile, the implementation degree of the "trade-in for new" policy and the implementation of emerging demand growth points will also play a significant role. Specifically, the capacity on the supply side has maintained a high growth rate, but the elimination of old facilities may also lead to a temporary narrowing of local supply. From the demand side, the accelerated integration process such as caprolactam and propylene oxide, as well as industries with low raw material matching rates like papermaking, will remain the main growth points for hydrogen peroxide demand. Meanwhile, the improvement in macroeconomic expectations and the increased demand from the policy end for other fields such as new energy may to some extent alleviate the downward pressure on the hydrogen peroxide market.

In 2026, the supply and demand contradiction in the hydrogen peroxide market will still persist, and the price may maintain a low and narrow range fluctuation trend. It is expected that the average price of hydrogen peroxide with a concentration of 27.5% across the country will fluctuate narrowly around the cost line, with limited ups and downs. The estimated fluctuation range is around 650 to 850 yuan per ton.